EU Digital Sovereignty And Digital Infrastructure

Europe’s Digital Sovereignty Push Is Redrawing the Digital Infrastructure Map

Digital sovereignty has rapidly evolved into one of the most consequential forces shaping Europe’s digital infrastructure landscape. What began as a niche debate about data protection and market power is now driving hard, capital-intensive decisions about where data is stored, the infrastructure design of data systems, and which regions will underpin Europe’s digital economy over the next decade.

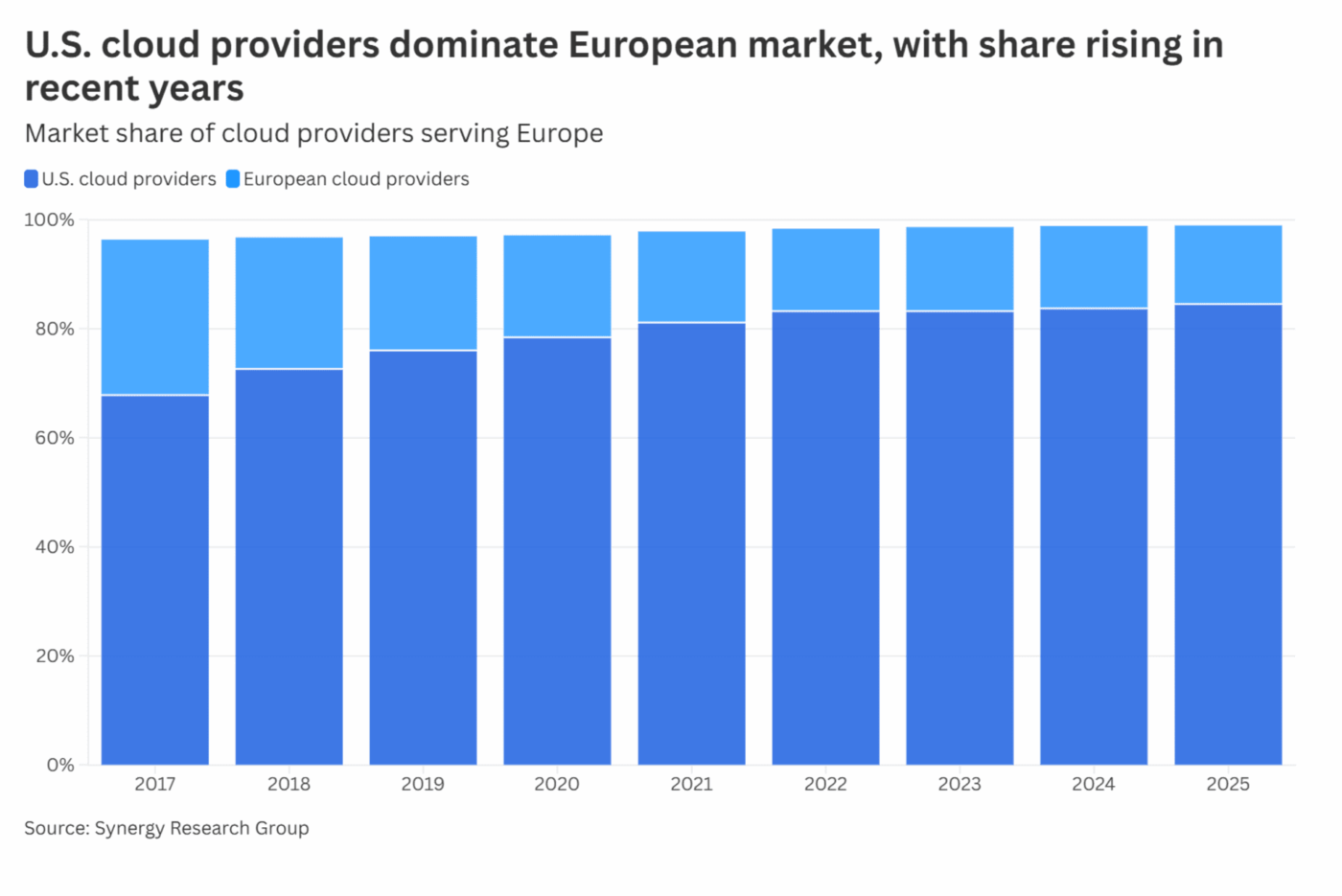

At its core, Europe’s sovereignty agenda reflects a growing discomfort with dependency. Estimates cited by EU institutions suggest that more than 80% of Europe’s digital products, services, infrastructure and intellectual property are supplied by non-EU providers[1]. In cloud services, for example, US providers dominate the market with over 80% market share[2]. For policymakers, this is no longer a benign outcome of globalisation, but as a strategic vulnerability.

The Franco–German summit on European Digital Sovereignty in late 2025 made this shift explicit. Its final declaration framed sovereignty as a cornerstone of Europe’s digital resilience, competitiveness and social model. The direction of travel was clear: more European control over data, cloud infrastructure and critical technologies.

From Policy Abstraction to Physical Reality

But what is digital sovereignty? The debate is often complicated by its abstract nature, with concepts that span several dimensions, including data sovereignty, operational sovereignty and technical sovereignty. However, at its core, it can be defined as the push for countries and jurisdictions to have “control over its own technology infrastructure, including that for storage and processing data” amid “growing concern over external dependencies and control”[3].

Although it is often considered in more abstract terms—such as increasing the proportion of Europe’s data that is stored, processed, and governed within European jurisdictions—Europe’s ambitions are ultimately reliant on the physical world. Data sits in data centres, connected by fibre and towers, powered by electricity and cooled by water. As such, in practice, this translates into a preference for local or regional infrastructure, even where global platforms may remain involved.

But this shift is not occurring in a vacuum. Europe’s digital infrastructure is already stretched. By the end of 2025, industry estimates pointed to limited spare capacity, with data centre vacancy rates in some hubs in the low single digits. At the same time, data traffic in Europe is estimated to be growing at 25% per annum to 2030[4], driven by cloud migration, streaming, enterprise digitisation and, increasingly, artificial intelligence.

Against this backdrop, sovereignty acts as a demand multiplier rather than a marginal factor.

The implications of Sovereign Rules and Security

One of the less discussed sovereign drivers for local infrastructure is digital regulatory divergence. The United States has traditionally favoured market-led self-regulation. China places national security and state oversight at the centre of its digital model. Europe, by contrast, has embedded individual rights and privacy into law, most notably through GDPR.

GDPR’s extra-territorial reach means any company handling EU personal data must comply with European rules, regardless of where it’s headquartered. In practice, this raises the cost and complexity of cross-border data transfers and increases the attractiveness of keeping data locally. Transatlantic frictions, exacerbated by US surveillance laws, such as the CLOUD Act, have reinforced this dynamic, hardening European scepticism about relying on overseas infrastructure.

Since the invasion of Ukraine, policymakers have also become acutely aware that digital infrastructure is strategic. At the heart of it, data is a critical national resource, central to continued economic and social development, national security and overall connectivity. Continued access and control are not nice to haves but necessities. This feature of the data sovereignty debate is succinctly highlighted by the Financial Times.

“A quieter, equally consequential battle is being fought in the cloud. As European leaders double down on “digital sovereignty” in the face of threats from the White House, Big Tech companies have performed a remarkable rebranding and are now marketing “sovereign solutions” encompassing AI, cloud services and data centres. Sovereignty, however, is an inherent right of democratic states, not a subscription model provided at the mercy of foreign entities.”

Furthermore, limits on continued access can be both physical and political. Cyberattacks, sabotage of fibre routes, and disruptions to power are no longer theoretical risks but are daily occurrences. Likewise, the risk of foreign actors limiting access for political reasons is now a reality, exacerbated by growing geopolitical tensions.

Localising data and digital infrastructure is therefore increasingly framed as a means of improving control and oversight, reducing exposure, and responding to threats.

Capacity Constraints and the Energy Bottleneck

The European Union has committed to a major expansion of data centre capacity by 2030, often framed as a doubling from current levels. Yet simple arithmetic raises questions about whether this will be enough. According to Savills, total international bandwidth usage in Europe is projected to increase at a compound annual growth rate of 31% to 2030.

Moreover, building data centres is only part of the equation. Energy availability has emerged as the binding constraint in many markets. Data centres already account for an estimated 3%[5] of electricity demand in several European countries, with projections suggesting this could rise to high single digits in concentrated markets.

Ireland offers a cautionary tale. Rapid data centre growth, unaccompanied by sufficient investment in energy generation and grids, is contributing to higher power prices, tighter supply for other users, and broader economic spillovers, including constraints on housing and industrial development. Sovereignty-driven growth risks repeating these dynamics elsewhere unless energy infrastructure is developed in parallel.

Beyond FLAP-D: A More Distributed Future

Historically, European data centre investment has clustered around the FLAP-D markets – Frankfurt, London, Amsterdam, Paris and Dublin. Today, those markets face converging constraints: land scarcity, power limits, water availability, and increasingly complex permitting.

The sovereignty agenda is accelerating a shift that was already under way. Secondary and tertiary markets, Poland, the Czech Republic, Belgium, the Nordics, and Italy among them, are attracting significant new investment. These locations offer combinations of available power, supportive regulation, skilled labour, and proximity to growing demand.

Cordiant is experiencing this first hand, through its exposure to the Czech market, where it is developing Prague Gateway, one of central Europe’s largest datacentres, alongside its existing datacentre business, as well as Poland and Belgium. In the Czech Republic and Poland in particular, this trend is supported by strong GDP growth, low unemployment, low debt to GDP and relatively low inflation.

A Defining Test for Europe’s Digital Ambitions

Digital sovereignty is now embedded in European policy thinking, extending well beyond privacy into infrastructure, industrial capacity, and geopolitics. Its impact on digital infrastructure will be profound and unavoidable. Demand for data centres, networks and energy will rise faster, spread more widely, and become more politically salient.

The challenge for Europe is execution. Poorly coordinated sovereignty policies risk creating parallel systems, higher costs, and new bottlenecks that undermine competitiveness. Done well, the same agenda could catalyse investment, strengthen resilience, and anchor the next phase of Europe’s digital economy.

For policymakers, investors and operators alike, the message is clear: digital sovereignty is no longer an abstract debate. It is already reshaping where capital flows, where infrastructure gets built, and which regions will carry Europe’s digital future.

[1] European Parliament – ‘REPORT On European Technological Sovereignty And Digital Infrastructure’

[2] Synergy Research Group

[3] Osborne Clarke – ‘How Data Sovereignty is Reshaping Business Strategies’

[4] Arthur Little – ‘The Evolution of Data Growth in Europe’

[5] Independent Commodity Intelligence Services – ‘Data centres: Hungry for power’